NOT YET OUT OF THE WOODS

FOR a spell last year American banks seemed poised to reattain the sort of double-digit returns that have largely eluded them since the financial crisis.

A robust market for takeovers and public offerings was producing a flurry of fees. Credit quality, which had collapsed in the crisis, was “pristine”, according to Jamie Dimon, the boss of JPMorgan Chase, America’s biggest bank by assets—something that was allowing banks to reduce the provisions they had made to cover soured loans. The rash of swingeing fines that had been disfiguring profits had largely dissipated (although Goldman Sachs recently agreed to pay $5 billion to settle charges that it knowingly peddled dodgy mortgage-backed securities). And then there was the Federal Reserve’s decision to raise interest rates in December for the first time in nearly a decade, which held out the prospect of a growing margin between the rates banks pay depositors and those they charge borrowers.

Glimmers of that sunnier outlook can still be seen in the big American banks’ annual results. JPMorgan Chase reported a record annual profit on January 14th of $24 billion. Bank of America and Citigroup posted their biggest profits since 2006 (although the return on equity at both is a fraction of what it once was). Yet share prices in the banking sector have fallen by more than 20% since July, with half of the decline coming in the first weeks of 2016.

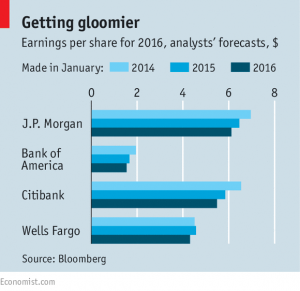

In part, the poor performance of bank shares stems from the broader gloom in global markets. But investors have also noticed that the growth in banks’ profits comes more from falling costs than from rising revenue. Worse, the trends that propelled profits upwards in 2015 appear to be reversing. Analysts have cut their forecasts for profits in the coming year (see chart).

The worsening outlook for the world economy has made markets much more sceptical that the Fed will continue raising rates. Whereas members of the Fed’s rate-setting committee predicted in December that rates would rise by a full percentage point this year, markets now expect an increase of only a quarter of a point. The prospect of higher lending margins, in other words, is evaporating. Yet December’s increase has curbed the hugely profitable business of refinancing mortgages.

The volatility in markets, meanwhile, is causing takeovers and issuance of shares and debt to atrophy. There is supposed to be a bright side to the turmoil, since volatility typically boosts trading revenues. But many investment banks have curtailed their trading operations under regulatory pressure. That has left them ill placed to capitalise on the turmoil. Banks have been beefing up wealth-management arms even as they curb trading, in the hope they will provide steadier profits at less risk. But falling markets also harm these, since costs are fixed but revenues come in the form of a percentage of the shrinking value of assets under management.

In addition, instead of reducing provisions, banks are now adding to them. The main culprit is the collapsing oil price, which is crushing energy firms. JPMorgan Chase, for example, set aside $124m in the final quarter of last year to cover any losses in its loans to energy firms.

None of these problems is fatal. According to Goldman Sachs, Citi has the biggest exposure to energy firms among banking behemoths, at a modest 3.3% of its loan book. Recent years have been lean in part because banks have been building up their buffers rather than racking up big profits. Although many banks struggle to earn a decent return, the number that are failing or in trouble is near a record low, according to the Federal Deposit Insurance Corporation, a regulator. For investors, however, that is scant consolation.